Historically, the market has only gone up by 5.7% per year.

I bet you thought it was more.

But, that's not the full story. When calculated in a different way, the historically-based number could be more than twice as much, at 12.1%.

Believe it or not, both figures—the 5.7% and the 12.1%—are entirely accurate.

And, I’ve seen them both used to mislead you (depending on what the speaker/author is trying to get you to do).

I’ll walk you through the math so that you’re as prepared as possible the next time someone’s trying to convince you one way or the other…

More...

Same Coin; Two Sides

If you’re working through your financial plan, you’ve been told some story about what “the market” has done in the past.

If someone is trying to convince you that you should have a greater sum in the market, you’ve probably heard that it has historically averaged 10%, or maybe even 12% per year.

On the other hand, if someone is trying to convince you that you should put your money elsewhere, you’ve probably heard a much lower figure, like 6%.

Well… which is it? Where are these numbers coming from and which should we use for our planning considerations?

The Market

First off, we should probably define "the market" as there are, in fact, many markets in the world of investments (we'll explore the most relevant to you over time). In most cases—in most finance-themed conversations where "the market" is mentioned—however, people are referring specifically to the stock market.

(Now, I’m assuming at this point that you have a basic understanding of what a stock is. If not, that’s okay, you can check out this old video.)

In an attempt to track the performance of the stock market as a whole over time, a few indices are relied upon.

The Indices

An index tracks a group of investments as opposed to just one individual stock. There are three major indices:

- NASDAQ 100

- Dow Jones Industrial Average (DJIA)

- S&P 500

If you follow stocks anywhere, you’ll see these three more than anything else front and center.

The NASDAQ (National Association of Securities Dealers Automated Quotations System) is generally thought of as representing the technology sector. In fact, however, it’s made up of the 100 largest non-financial (not just tech) companies. It can provide a fascinating insight into the rapid growth of many of the most innovative companies in the world. But, it’s not a good representation of the entire stock market.

The Dow is made up of companies from all different sectors, but… only 30 of them. No matter how large each is, that’s hardly a large enough subset to give us the best glimpse into the performance and health of the stock market (in fact, it’s kind of just used as a token measure at this point…).

The S&P 500 is made up of the 500 largest US companies—which represents roughly 80% of the total US stock market. (source)

So, quiz time…

Which of the three most common indices do you think would provide with the best insights into the performance of the market as a whole?

...if you didn’t say the S&P 500, I’d love to know why!

Anyway… I have on occasion (and if you’ve read or watched enough financial content you probably have as well) seen ‘experts’ use the DJIA as their measure for stock market returns.

Word of Warning

That 30-company index is obviously not as good a measure—not as comprehensive a representation—of large US companies.

Why, then, would anyone use it to demonstrate the stock market’s historical returns?

Either...

- He just wasn’t thinking, didn’t know any better, and happened to have his Dow 30 historical data more easily accessible than the S&P 500, or…

- He has an agenda.

It’s not severe, but every percentage point makes a rather significant difference here (as we’ll explore in detail in upcoming posts).

Averaging the returns of the DJIA from 1926 through the end of 2019 produces an average annual return of more than 2%-lower than the S&P 500’s.

We could even just keep adjusting that starting date (it debuted in the late 1890s) until we found an average return that was even lower—see how easy this business of data manipulation is! Instead, however, I chose 1926 so that it would coincide with the start date of its S&P counterpart. (You can play with the calculator here.)

If someone wanted to be really tricky (and I have seen this, so be careful…), they’d produce for you this same figure without factoring for reinvested dividends.

Dividends

A dividend is a sum of money paid regularly (typically quarterly) by a company to its shareholders out of its profits or reserves. Many of these large companies (in the Dow 30 and the S&P 500), have a long track record of paying dividends.

Aside from a stock's value going up over time, this is the other primary way shareholders stand to profit from their investment.

Obviously, any dividends that have been paid out should be considered in these calculations of your average annual return. They do benefit you along the way.

The easiest way is to just assume they’re reinvested (most calculators will do that for you).

With clever wording, however, I’ve seen some ‘finance gurus’ get away with the omission just to prove their point.

Consider this: “Historically speaking, the share price of the collective companies within the Dow 30 (ie the price of the index) has averaged less than 6% per year!”

See what I did there?

That was all true!

...albeit extremely misleading.

Leaving this one consideration out of the Dow’s historic calculations produces an average annualized return of just 5.7%.

Tricky, tricky… just like that, we’ve already cut some average annual return claims by more than half. All while using very real historical data!

It’s not hard to imagine someone taking that previous claim and stretching it into something like: “historically speaking, the market has actually only averaged less than 6%,” and feeling okay with the fact that everything they just said was technically true (if not upsettingly misleading).

My point with this—my caution to you—is that it’s not hard to prove a point one way or the other here.

Our Approach

You can’t just hear a figure that sounds convincing and take it at face value. You'll find this type of manipulation on all sides of most financial issues.

My goal is to take you through my own journey of truly understanding the long-term implications of these numbers—of each tenth of a percentage point in this case—of understanding what figures are truly relevant to myself and my clients and which ones are misleading.

I’ll be taking you through that process—exposing misconceptions wherever they are.

Long story short: I’m with you on a constant quest for truth here. It’s because these truths have been invaluable for the viability of my own and my clients’ financial plans that I create resources like this. After discovering and understanding financial truths, only then do I seek the best solutions. I strive to be ever-open-minded and hope you’ll do the same.

Okay. Cautionary rant over.

Obviously, we won’t be using the DJIA on this one. We’ll stick with the S&P 500.

The S&P 500

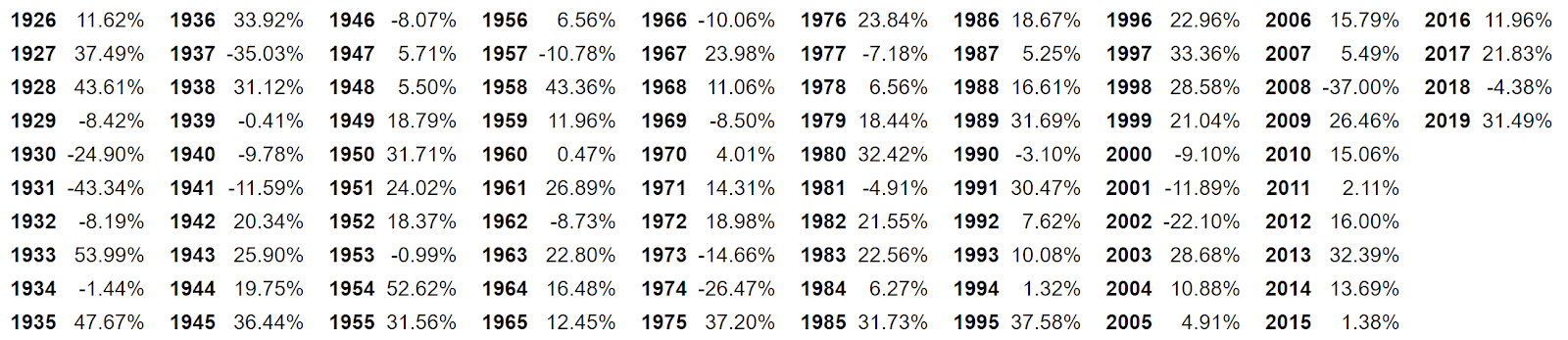

Originally consisting of 90 of the largest companies in the United States, Standard & Poors started tracking this index back in 1926. In 1957, it was expanded to the 500-company composite we recognize today.

Here’s the year-by-year return breakdown:

To calculate a simple (or arithmetic) average, we just need to add all these returns together and then divide by the number of years (94). This calculation reveals that from 1926 through the end of 2019, the S&P 500 has averaged a 12.1% annual return.

Boom!

There you have it. Case closed! 12% per year is what you should expect in the market.

It’s true: the simple average of the market’s annual returns comes out to 12.1%!

Although some people (think: Dave Ramsey) might like to just stop there...

You shouldn’t!

This is still not even close to the full picture of what you should expect from the market. But, at least you know...

- Which index to look toward for some real historical insight.

- And, to question anyone that’s using Dow statistics.

In our next post, we’re going to explore what the actual historical return of the market has been, because… it’s not 12%.

Sorry, Dave.

One of the best ways to keep up with all the valuable content we're creating is to subscribe to our YouTube channel and click that pesky notification bell.

And, if you’re sincerely interested in understanding some of the problems I’ve discovered with the financial industry, you should check out our private community.

I hope to see you in there! Regardless, I wish you all the best.

Take care.