There are some advisors and (loud) financial voices out there who are still promoting the use of mutual funds in your investment portfolio...

We’re going to break down and explore just how expensive they really are and the impact mutual fund and exchange-traded fund fees have on your portfolio’s long-term performance...

More...

In our last post, we explored the significant impact advisory fees can have on your bottom-line.

It was pretty alarming, right?!

Where, just due to an industry-average advisory fee of just 1%, after 30 years your account was only 44% your initial projections.

Now, let’s take this honest exploration (that we’ve been undergoing over these last couple of weeks) of actual returns that you can realize in the market one step further...

FUND FEES

Think about where these broker-dealers and RIAs (registered investment advisory firms) are ultimately investing.

Most will invest in mutual funds and exchange-traded funds (ETFs)—both of which bring with them yet another layer of fees (the former much more significant than the latter).

Even when your firm invests some of your money in individual stocks (thus, not incurring a fund’s fees), they tend to find a way to hurt your bottom line regardless—Edward Jones, for example, will charge you a ~2% commission and Northwestern Mutual just has a flat (and relatively high) trading commission that is automatically pulled from your account every time your rep puts you in or out of an individual stock position (which is even more destructive on smaller accounts).

But, back to the funds… Let's start with Mutual Funds.

Mutual Funds

Mutual funds are investment programs where investors are essentially pooling their money in order to allow a money manager to diversify their holdings.

Vanguard, BlackRock, Fidelity, and American Funds are by far the largest mutual fund families in the world—each boasting more than $1.5T in assets.

While BlackRock is contending with Vanguard on the ‘low fees’ front (don’t worry, they’ll come up again later), Fidelity and American Funds continue to rock some pretty hefty charges.

Northwestern Mutual’s go-to fund provider is the old-guard behemoth, American Funds. Part of the reason for this is because with these higher fees that they're extracting from investors, American Funds is able to offer a larger cut to middlemen—e.g. Northwestern corporate and the individual agents (their ...sales reps).

However, with Vanguard, for example, and its lower fees there isn’t as much to share. Thus, during my Northwestern tenure, I became very familiar with the American Funds fee structure.

Share Classes

Advisor-sold mutual funds often have different options for how you’d like to structure their fees. These different options are called share classes.

- A Shares will charge a large front-load fee. And then, they have lower on-going fees: for marketing and operating expenses.

- B Shares (not very common) charge a back-end load and come with higher on-going expenses.

- C Shares are considered to have a “level” load—there’s no front-end charge, they (generally) have a much lower back-end fee, and their operating expenses are relatively higher.

A and C shares tend to be the most common among retail investors (that’s the industry term for the non-professional investor). Let’s start by exploring the latter with its level annual fees.

Quick note: If doing this digging yourself, use caution to look for the total net annual expense ratios and not just the management fees. The total expense ratio is always larger than the management fee alone (even if that difference is, for some funds, negligible).

American Funds’ largest fund is the Growth Fund of America (AGTHX) with $115B in assets. The net annual expense ratio for C Shares is 1.4%. (source)

Obviously, another 1.4% hit to our sum (from our last post) would be significantly impactful—as it would be for your long-term returns, if that’s how you’re invested.

There are some advisors (even some I know personally) who will simply plug you into a portfolio of American Funds funds and charge you their own (significant) advisory fee on top...

A 1% advisory fee + a 1.4% fund fee is crazy destructive to your bottom line!

But, to be fair, most don’t do that.

...most!

Most of the advisors with those larger firms utilize a mix of mutual and exchange-traded funds.

Exchange-Traded Funds (ETFs)

An ETF is a security derived from a collection of stocks (usually) that often track an underlying index (e.g. S&P 500, DJIA).

Because the funds’ underlying holdings are based on whatever its respective index is doing rather than rigorous research from a team of (expensive) professionals, the expense ratios are considerably less—as low as just two one-hundredths of one percent. (source)

(I think there was one with a negative fee… but… I’m pretty sure it just shut down. Who’da thought?)

With that mix of mutual and exchange-traded funds, the average additional fee incurred by those larger advisory firms (the RIAs and broker-dealers cited in our last post) is around 0.4% (some quite a bit more, some even less). (source)

So, that’s an additional on-going fee and should be considered in your expectations.

Even though there are several examples of large players in this space (cough, cough... Ameriprise Financial—see our last post) who incur higher fund fees on their clients’ hundreds of billions of dollars that they have under management, we’ll stick with that 0.4% average (and we’ll assume a low advisory fee of just 1%).

Let’s refer back to that same example we used in our last couple of posts...

Remember that $100 invested in 1926—that would have been projected to grow to $4.6MM with the 12.1% assumption but then, in reality, turned out to be less than $1MM?

Well, after accounting for those advisory and fund fees, your ‘since-1926’ number would actually only have grown to $254,000—5.5% of your original expectation.

- Your 10-year return would be 73% of its projected value

- Your 20-year return would be 54% of its projected value

- And, your 30-year return, only 40% of its projected value

Remember: the advisory and fund fee assumptions that we’re using here are average. That means that there are tens of millions of investors out there who, even if everything goes as planned (read: the market actually does what it did in the past...), they’ll be facing an even harsher reality than those we just considered.

Know where you fit in and adjust your expectations accordingly.

A Shares

Now, let’s explore the differing impact that A Shares should have on your return expectations. A Shares for The Growth Fund of America come with a hefty 5.75% front-load fee.

The on-going fee would then be 0.65% in this case (it varies by fund, whereas the front-load is generally the same).

This equation means you are immediately down almost 6% on Day 1 of your contribution into this fund.

A case could easily be made, however, to mathematically show you how much better off you’d be (than with its C-Share counterpart) over the long run for making that initial sacrifice.

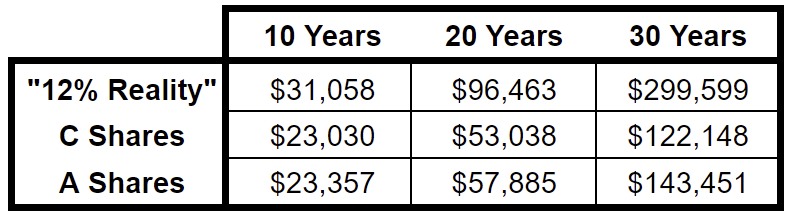

Here is a breakdown of how a $10,000 investment would look after 10, 20, and 30 years given the actual historical return of the market.

I’ve accounted for no advisory fees here—just the up-front 5.75% plus the on-going 0.65% fees for A Shares and the annual 1.4% fee for C Shares. (And for the additional emphasis, I’ve placed them both beside that 12% historical market average—or the “12% Reality” as Dave Ramsey calls it.)

With historical market returns, it would take just under 9 years for the growth of that $10,000 invested into A Shares to pass its respective value in C Shares.

You can see how easy it would be to convince a young person trying to ‘do the right thing’ and save for the long haul to splurge for the A Shares’ front load.

Whether this is actually a good idea for you or not really depends on you and what your plans are. Sure, you’re committed to investing for retirement, which may be a decade (or two or three) from now, but are you that committed to this particular fund?

ALL TOGETHER NOW

Think back on Dave Ramsey’s reassurances (as discussed in this post) about your ability to realize 12% in the market.

In that same “12% Reality” article, he encourages you to invest in mutual funds (ideally, front-loaded with an expense ratio under 1%, he says) (source) and to use one of his ‘experts’ (...we’ll definitely be evaluating them more in a future post).

When you factor in all of this—actual (instead of average) returns, advisory fees, and fund expense ratios—you will be hard pressed to realize even an 8% annualized return under the historical assumptions these market peddlers love to cite...

The two personalities mentioned (in this post and our last) are major influencers of everyday Americans just trying to save for their retirement goals...

- Dave Ramsey with his more than 14MM weekly listeners and more than 11MM books sold.

- Ric Edelman with his firm’s more than 1.2MM clients.

Testing the 'Experts' Models

Let’s look at what those everyday Americans saving for retirement would have actually realized over the last 10, 20, or 30 years compared to the expectations laid out by these men (and so many others).

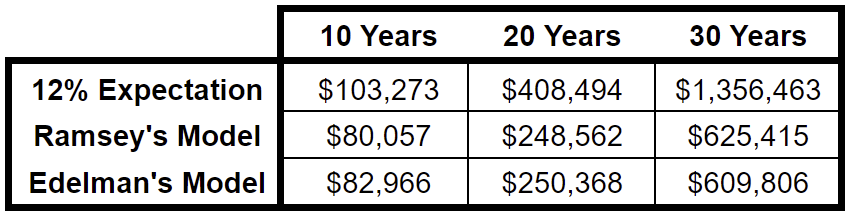

For Dave, we’re assuming here...

- a conservative advisory fee of 1% and...

- a more-than-acceptable (by his standards) annual fund fee of 0.65%...

- with a 5.75% front load (the actual fees of American Funds’ most popular fund).

For Ric, we’re assuming...

- that 1.75% advisory fee that his firm charges to accounts under $400,000 and...

- the low end of his firm’s average underlying fund expenses, 0.3%.

Assuming actual (geometric) average historical market returns and a $5,000 annual contribution, here is how far off your reality would be from that 12% expectation they’ve both set:

At 12%, after 30 years, an account would have grown to more than $1.3MM...

- Using Ramsey’s guideline assumptions, you’d have less than half of that.

- With Elderman’s, you’d have even less with just over $600,000.

A far cry from Dave’s ‘real 12%’ (despite all his comforting words of reassurance along the way) and Edelman’s ‘conservative’ 12% (with that 14% expectation seeded in the back of many readers' minds).

Robo Alternatives

Now, real quick, it may sound, at this point, as though I am simply advocating a more automated (read: anti-fee) approach.

After all, for most of these advisors (really, sadly, almost every single one of them…), you’re paying all these fees for them to just plug you into the same old stock-and-bond-only, buy-and-hold approach that you could find somewhere else for way less!

Sure, some of them might have their own little twist (most don’t) or claims of added value, but if you buy into that stock-and-bond strategy, why wouldn't you just go with one of the far-less-expensive alternatives who will just plug you right in at a fraction of the on-going fees?

You have your broker-dealer options, like Vanguard or Charles Schwab with their negligible advisory fees (0.30% & 0.28%, respectively).

Or, there are the robo-advisors, Betterment and Wealthfront (both at 0.25% at the time of this writing).

This is, in fact, not the route I would recommend, but for reasons we’ll cover in due time.

...sorry, but there’s a lot to unfold here!

We’ll explore all of this in greater detail later (the value of the advisor expertise for which you’re paying; the validity of the buy-and-hold, stock-and-bond-only strategy), but with all this discussion of fees, these low-cost players deserved a mention here (even if you still can’t count on a 12% return).

Besides, I’m sure many of you reading were screaming about these low-fee alternatives already. I just wanted to assure you: I’m not ignoring them.

Okay, fine, so back to the main theme here of trying to determine what returns should you actually expect from the market...

MORE COMPLICATED STILL

We just use this adjusted historical return figure to manage our expectations then...

Right?

We came down from the simple average of 12.1% to the real average of 10.2%.

And then, after accounting for average fees, the real historical return of the market dropped to 8.7%.

That’s it—that’s the figure we should use now, right?

Easy enough…

So, we just need to save more or prepare for less…

Unfortunately, it’s still not that easy.

The reality is significantly worse…

But, it’s too much for one post.

... Sorry!

I know that’s a terrible cliffhanger, but it’s the truth.

One of the easiest ways to keep up with the value we're creating for you is to subscribe to our YouTube channel and hit that pesky notification bell.

If you’d like more from me and my team, check out our private community.

Until next time…

Take care!